Saving in the age of abundance

Can software save savings? New thinking for a world with negative real interest rates.

With today's zero or negative real interest rates, deciding what to do with your cash and short term savings has never been harder.

Savings accounts at major banks have paid close to 0% for nearly a decade, but now even online banks, credit unions and cash accounts from fintech startups pay 0.6% at best. CDs, "high yield" checking, and money market accounts are no better and come with even more restrictions. Treasuries? 1 month and 1 year T-Bills also pay near zero. Bond funds? Expense ratios, changing prices, default risk and minimums make these too complicated for the typical saver. What about peer-to-peer lending sites like Lending Club? These generate what seem like good returns, but it's hard to overstate the risk. You're making loans to people or businesses that didn't qualify for a loan from a traditional lender.

After exhausting all these options, you might just give up and decide to play the lottery with your savings. Since 1956, the UK government has offered Premium Bonds, where interest for bond holders is determined by lottery. This gamified experience is one of the top savings vehicles in the UK, where about one third of citizens hold bonds valued in total at over $100 billion. A startup named Yotta just graduated from Y Combinator's Summer 2020 batch to launch a similar business in the US, and PoolTogether raised a seed round led by IDEO Colab Ventures early this year for a blockchain-based version. Of course, these models are based on lotteries. They're gambling. Most people receive nothing, and any expected value calculation would tell you this game is not worth playing.

Are savings options so bad that people would rather gamble for the remote chance of winning some interest than even be bothered with a traditional savings vehicle?

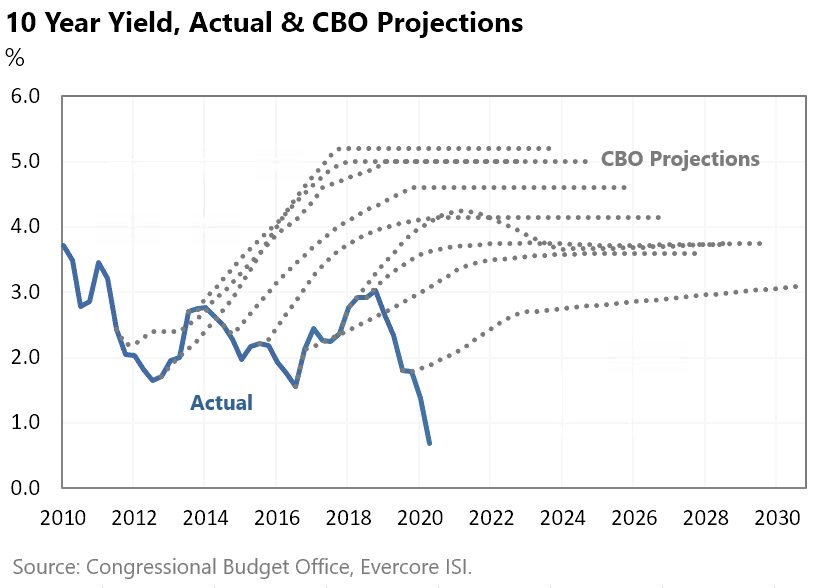

Why have rates been so low for so long? Is there any end in sight?

Age of Abundance

Technology and digitization are driving incredible improvements in global quality of life, moving the world from an era of scarcity into an era of abundance.

Thirty years ago, finding an answer meant going to the library to read some books or asking people you knew. As of 2016, Google had indexed 130 trillion web pages, providing instant answers to anything for everybody. Information is no longer scarce, and what's now scarce is matching the best answer to a question. Alex Danco calls this positional scarcity.

Similar technology-driven processes of commoditizing supply and aggregating demand are playing out in industry after industry, giving rise to natural super-monopolies. Amazon has done this first in books, then in all retail. Netflix has done this in entertainment, Airbnb in accommodation, iTunes and Spotify in music, Facebook in your personal life, and Linkedin in your business life. The list goes on and on, and this software eats world process is still in the early innings.

The dark side to all this abundance is that technology is generating a Moore's law fueled deflationary cycle. Technology gives you more for less. This, by definition, is deflation. The faster technology spreads throughout the economy, the more deflationary pressure there is. In 2009, Microsoft was the only technology company in the top ten S&P 500 companies by market cap. In 2019, the top five companies in the S&P 500 by market cap were all technology companies. Humans, by nature, find it extremely difficult to see and understand exponential growth even when it is happening right in front of them.

If you want to test if you have a good feel for exponential growth, Jeff Booth in his book the Price of Tomorrow, asks a simple question. He says "Imagine if I fold a piece of paper on itself fifty times. (I can only fold it seven times before it resists too much, but let’s assume for the moment that I can keep folding it up to fifty times.) How thick would the piece of paper be on fold fifty?"

I've never met anyone with a gut feel for exponential growth. You always have to calculate it. But everyone in the startup world at least knows never to turn their back on it.

— Paul Graham (@paulg) March 4, 2020

Most people give an answer of a few inches, and on rare occasions Jeff says he hears "to the ceiling" unless someone has heard the question before. The correct answer is that on fold fifty the paper would reach all the way to the sun (93 million miles).

But getting more for less seems great, right? What's the problem?

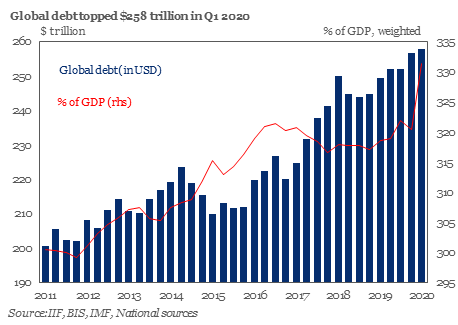

Consumer spending accounts for 70% of the US economy, and therefore growing the economy is heavily dependent on increasing consumer spending. But a steadily increasing deflationary force pushes consumers to spend less. And to get consumers to spend more, central banks lower interest rates to make borrowing cheap. This is why global debt has doubled over the last ten years.

In past situations, lower interest rates led to increased consumer spending which led to inflation, steadily decreasing consumer debt burdens. This is why the Fed has an inflation target of 2%. The US economy is built on credit and assumes a steady low level of inflation to work properly. But with strong deflationary pressure, inflation has proven elusive.

What happens in an economy experiencing deflation? The cost of debt in real terms increases and there is downward pressure on wages. This means your mortgage or rent payment gets steadily more expensive in real terms at the same time that layoffs and unemployment increase because employees also get steadily more expensive (and don't respond well wages cut). The higher the debt level, the worse this situation is. And global debt levels have never been higher.

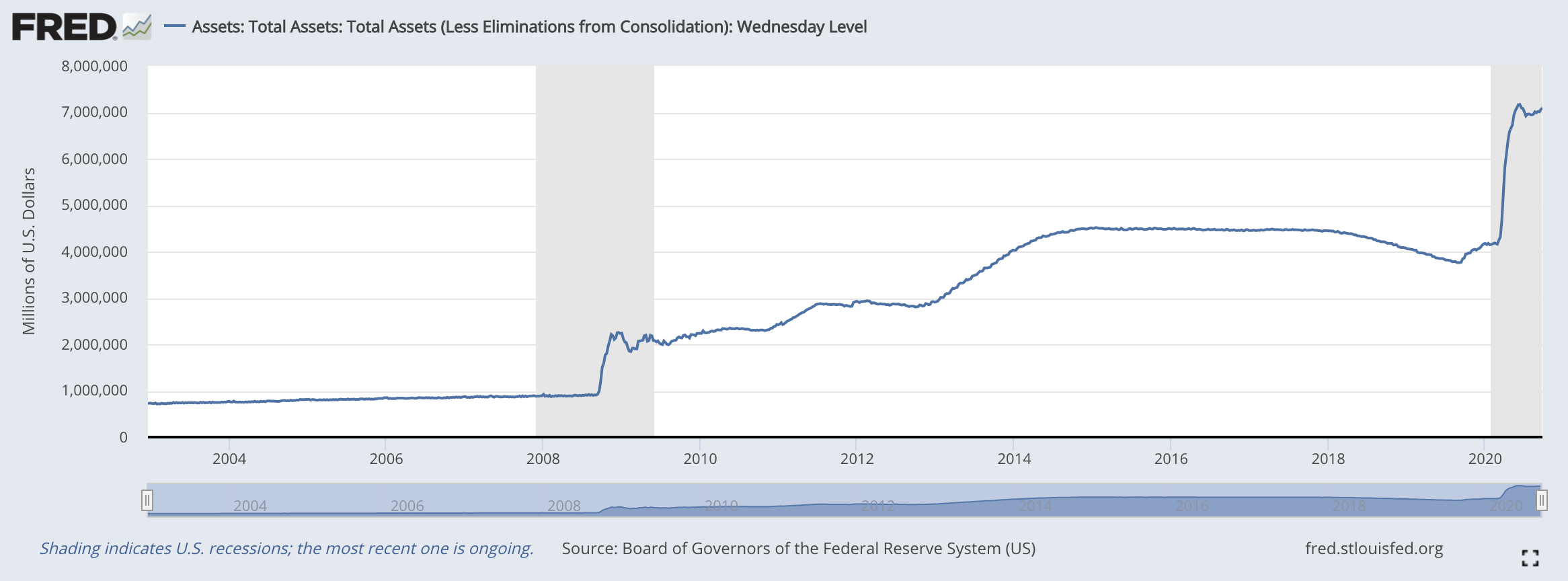

Left unchecked, this results in large-scale social unrest, populism, or worse. This explains why interest rates have been steadily decreasing for years and why the Fed has signaled they will keep interest rates at zero until at least 2023. And because zero interest rates are no longer sufficient to encourage enough new borrowing and spending, it's why Fed Chairman Jerome Powell said in March that there is no limit to the amount of money the Fed is willing to put into the economy to keep it afloat. The Fed continues to massively expand the supply of US dollars.

Understanding the fight between the exponential force of technology driven deflation and the inflationary forces of low interest rates and massive expansion of the money supply is important to understanding what is likely to happen to the future for interest rates and the yield on savings vehicles. With every doubling in the exponential spread of technology, deflation is harder and harder for governments and central banks to counter-act. This is a massive problem, but we'll leave that for another day. For our purposes related to savings, what's clear is that zero yield is probably here to stay.

Is there nothing we can do to save savings? It seems unreasonable to receive no compensation for letting someone borrow your savings. And even worse to have to pay for the privilege.

Savings accounts seem rather boring, like a long forgotten banking backwater. But what if we were to reimagine the savings account for the software century? Could we redesign them from first principles for the age of abundance? Could we unbundle them from the bank, strip out their costs, give them full transparency, and generally make them 10x better?

Let's try.

Can software save savings?

Before we start, let's make sure we understand the problem we're solving. What are savings accounts specifically for? And what jobs must a savings account do?

Savings accounts are designed to be used for expenses expected over the next year or so. These expenses might include emergency funds, property taxes, estimated income taxes, home maintenance expenses, home improvement expenses, car maintenance expenses, weddings, travel, and maybe clothing or gift expenses, among others. Savings accounts are not designed for monthly or bi-monthly expenses (that's what checking accounts are for) or for expenses expected to be more than 3-5 years away (that's what investment accounts are for).

With that in mind, let's break down the jobs to be done for a full service savings account:

- Keep your money safe

- From theft

- From being accidentally lost

- From bank run or default (e.g. FDIC insurance)

- Allow you to deposit money

- Electronically (intra-bank, ACH, wire, check)

- Cash (ATM, branch)

- Foreign currency (branch)

- Allow you to withdraw money

- Electronically (intra-bank, ACH, wire)

- Foreign currency (mail, branch)

- Provide overdraft protection for checking accounts

- Provide a ledger of all your transactions as a reference

- Provide separate logical account buckets to save for different expenses

- Provide compensation for the use of your money

As you look at these jobs to be done, can you identify a customer-first focus in how banks have prioritized them or what they have optimized for other than enriching themselves? I can't. Banks might pat themselves on the back for adding mobile account access or mobile check deposit, but the truth is that savings products have scarcely changed in decades, have evolved by incrementalism, and have never had a bottoms-up re-assessment. It reminds me of the wireless industry before the iPhone.

If we took a customer-first focus to re-imagining the savings vehicle, what jobs would we optimize for? Here's a list and how we might prioritize them.

- Reasonable yield. Savers want to be compensated for lending their money. They're upset when they learn that financial institutions make money on their savings while they receive nothing.

- Reasonable preservation of principal. Most savers need their money over the next year.

- Safety from theft, loss or default. Savers need to have confidence that their savings won't be stolen, lost or defaulted on by an insolvent institution.

- Electronic withdrawals. Let's assume customers have a checking account elsewhere so we can focus solely on ACH and internal transfers.

- Electronic deposits. Again, assuming a customer has a checking account elsewhere allows us to limit our focus to ACH and internal transfers. Notice that we optimize withdrawals ahead of deposits, the opposite of banks.

- Mobile only account management, analytics, and goals. Neo-banks have made some good improvements in numbers 4-6, but make no impact on the top jobs we want to optimize for.

Now that we know what we're prioritizing, let's think through how we might achieve our goals.

Yield and preservation of principal

I have a hypothesis that today's one-size-fits-all savings vehicles over-index on preservation of principal for many savers. What if savers might be willing to assume a small and contained risk of principal in exchange for better yield?

Most savers expect to need their money over the next year, but it's not like a checking account where they expect to need the money in the next 30 days. What if savers could pick from vehicles that hold their value as 93-95% in cash and 5-7% in another high yield or high growth asset? The high-yield or high growth portion could be many things, including corporate bonds, consumer loan portfolios, real estate, farmland, high dividend stocks, Bitcoin, technology stocks, or any portfolio combination.

With this approach, in the worst case scenario, a saver can be certain that under no circumstances is there less than 93-95% of principal when savings need to be withdrawn. In return, dividends or excess appreciation are paid and the account is re-balanced with a ratchet that does not permit re-balancing below a floor of 93-95% of contributions. While there is no guarantee of yield, this approach does allow your money to work for you and is certainly better than playing the yield lottery.

But what about the cost of managing these vehicles? Won't that require fees that eat into the yield? And what about safety and security? And the countless other expenses that banks have?

A totally different cost structure

What if our savings vehicle was not actually a savings account at all, but a multi-sided network that connected savers and yield managers? Savers put up capital with the goal of receiving the best possible yield subject to a hard floor for loss of principal. Yield managers compete against each other for savers and receive a small carry on yield generated. Once bootstrapped, this system can operate much more efficiently and at much greater scale than a stand-alone alternative.

But how do you get savers to trust the network and the yield managers? And how do you get yield managers to trust the network with their livelihoods? A company trying to launch this network would have significant trust hurdles, and acquiring supply (yield managers) and demand (savers) would be very expensive.

What if our multi-sided network was built around a savings protocol for assets locked in smart contracts? A savings protocol built on the public blockchain where the rules for keeping your money safe are encoded in software and there is full transparency on what these rules are and what yield managers are doing? A simple vehicle built using 93% cryptodollars and 7% Bitcoin is not at all far-fetched with technologies that exist today.

And because this savings vehicle is not actually a savings account, it doesn't need to be affiliated with a bank. That's good, because bank charters are expensive and come with onerous regulations. Of course, that does mean this savings vehicle is not FDIC insured. But does that matter? How can we be confident that our funds are safe from theft, loss or default?

A correctly designed public blockchain is more secure than any bank, and an open-source protocol with codified rules prevents any commingling of funds or possibility of default. For these reasons, I think it's safe to say that FDIC insurance is unimportant. That said, it could makes sense to include insurance against other bugs/errors through a service like Opyn. This could be paid for by either the saver or the yield manager.

Because this savings vehicle is a self-organizing multi-sided network, all the traditional fixed costs of a financial institution bears go to zero and the variable costs paid by network participants drive the entire system.

Governance and getting started

We've talked about approaches to yield, preservation of principal and safety from theft or default, but we haven't talked about how to handle withdrawals, deposits and the mobile interfaces needed by both savers and yield managers. Who is going to build and maintain that? Who will decide when changes are needed for the core savings protocol? And who will implement them? Without this, our savings vehicle will never get off the ground. And though the marginal cost of servicing one additional user is zero once the software is built, it's still an expensive fixed cost that must be paid in advance. And the network still needs to be bootstrapped like any other multi-sided network or marketplace business.

What our savings vehicle needs is an alpha player who raises capital to build the necessary software and to bootstrap the network. This player (or likely startup), its investors, and other key network participants should receive governance tokens that allow voting on all software changes to the network and provide rights to a small percentage of yield manager cash flow in exchange for their work supporting the network. To be clear, this fee should be small relative to the amount earned by a yield manager. There are many ways to think about token distribution, ranging from the traditional VC-style to the recently popular community owned fair launch.

Conclusion

Today's big banking model is built around bundling and cross-subsidization. But in a digital world, money moves as fast as information and competitors are just clicks away. As Jim Barksdale said, there are "only two ways to make money in business: One is to bundle; the other is unbundle." And there is an entire ecosystem of competitors unbundling the bank.

But today's bank competitors are mainly innovating around the edges. To truly make a difference, you need to innovate at the core.

It might seem like today there are no good options for your savings and that you're better off playing the interest lottery. But this should not be the case. There is no reason this can't be fixed, and every reason to believe it will.

All the pieces are there. Waiting to be put together. Waiting to change the world.

Who will answer the call?

Will you?

Did you like this article? Subscribe now to get content like this delivered free to your inbox. Learn more about what I do: https://andyjagoe.com/services/

Photo by Almos Bechtold

This newsletter is provided for informational purposes only, and should not be relied upon as legal, business, investment, or tax advice. You should consult your own advisers as to those matters. This newsletter may link to other websites and certain information contained herein has been obtained from third-party sources. While taken from sources believed to be reliable, Software Eats Money has not independently verified such information and makes no representations about the enduring accuracy of the information or its appropriateness for a given situation.

References to any companies, securities, or digital assets are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services.

Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Content in this newsletter speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.